Every time you walk into a doctor’s office, you’re not just there for treatment-you’re also entering a financial agreement. And for too long, patients have been blindsided by surprise bills, forced into high-interest financing, or pressured into handing over credit card details before even getting care. That’s changing. In 2024, New York State passed three groundbreaking laws designed to shield patients from predatory financial practices in healthcare. These aren’t just bureaucratic updates-they’re real protections that affect how you pay, consent, and get treated. And if you live in the U.S., this matters to you, even if you’re not in New York. Because this is the direction the whole country is heading.

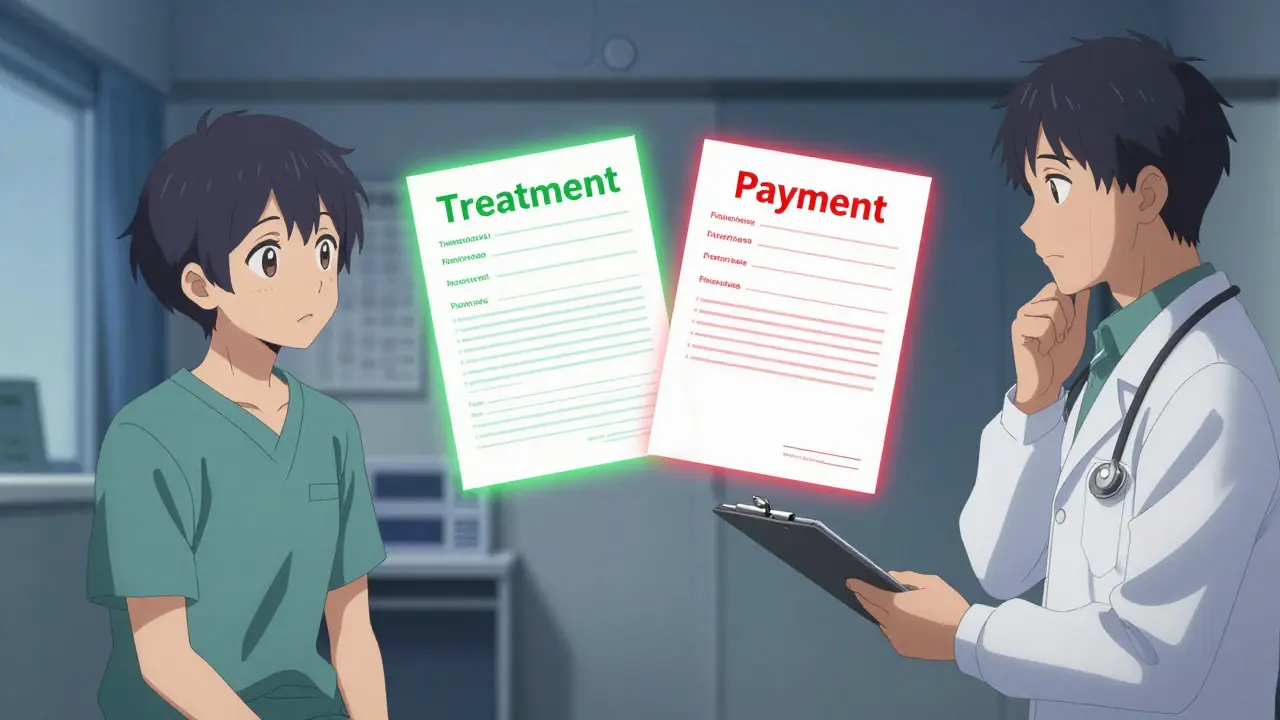

Separate Consent for Treatment and Payment

For years, patients signed one form at the front desk: a single signature that gave permission for both medical care and payment collection. That form was buried in a stack of paperwork. Most people didn’t even read it. But under New York’s Public Health Law Section 18-c, that’s over. As of October 20, 2024, healthcare providers must get separate, explicit consent for treatment and for payment. You can’t sign one box and accidentally agree to let them sell your debt to collectors or enroll you in a financing plan.

This means if you’re getting an MRI or a surgery, the provider has to ask you separately: “Do you consent to this procedure?” and then later: “Do you consent to how we’ll collect payment?” If they don’t, they’re breaking the law. And the penalty? $2,000 per violation. That’s not a warning. That’s a fine meant to force change.

But here’s the twist: as of August 2025, enforcement of Section 18-c was suspended. That doesn’t mean the law is gone. It means providers are waiting for clearer guidance from the state. So right now, you might still see the old forms. But if you’re asked to sign one document for both care and payment, you have the right to say no-and ask for separate consent forms. Don’t be afraid to push back. This is your right.

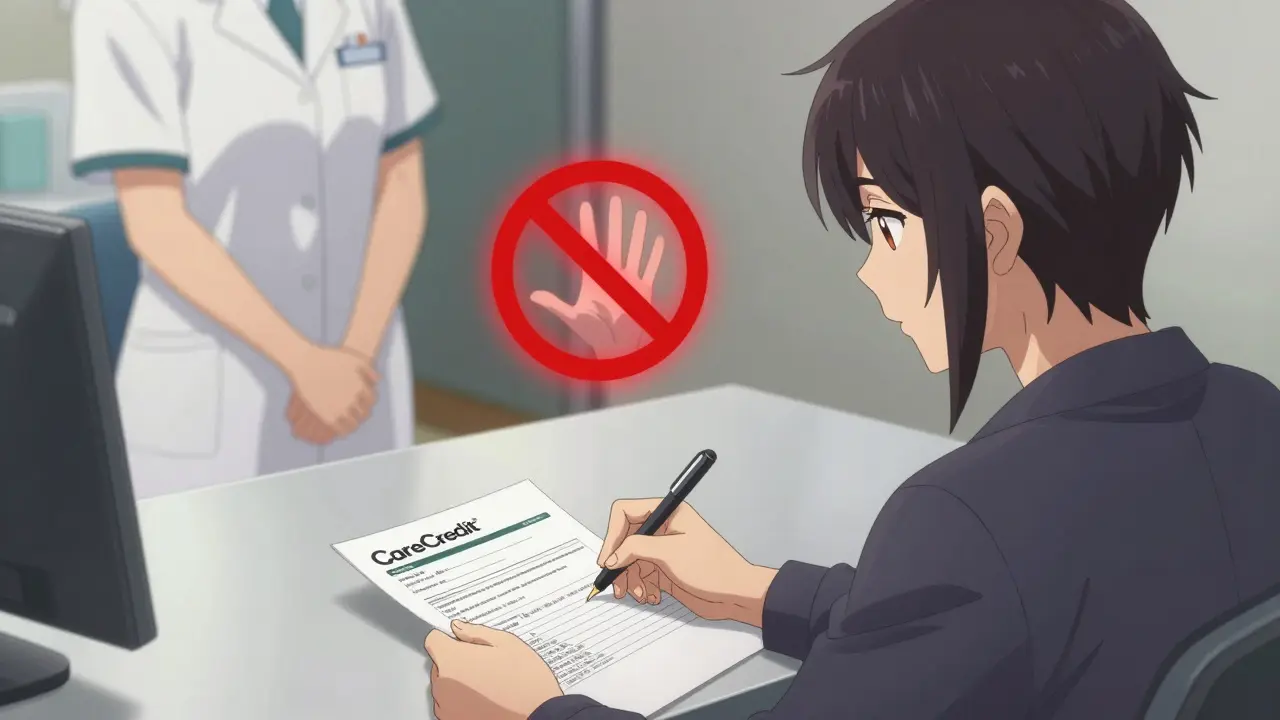

No More Filling Out Your Financing Applications

Have you ever sat in a waiting room while a staff member quietly helped you fill out a CareCredit® application? Maybe they said, “I’ll just check this box for you-it’ll make it faster.” Sounds helpful, right? Wrong.

Under New York’s General Business Law Section 349-g, healthcare providers are now banned from completing any part of a patient’s application for medical financing. Not even one box. Not even if you ask. They can answer questions. They can hand you the form. They can explain the terms. But you have to fill it out yourself. The law was written to stop providers from pushing patients into high-interest loans they don’t fully understand.

Why? Because medical financing products like CareCredit® often come with deferred interest. If you miss a payment or don’t pay off the balance in time, you get hit with years’ worth of back interest-all of it added on top of your original bill. And providers? They get paid upfront. You’re left holding the debt.

This law puts the power back in your hands. If a staff member tries to help you fill out a financing form, politely say, “I’ll do it myself.” If they insist, you’re within your rights to report them to the New York State Department of Health.

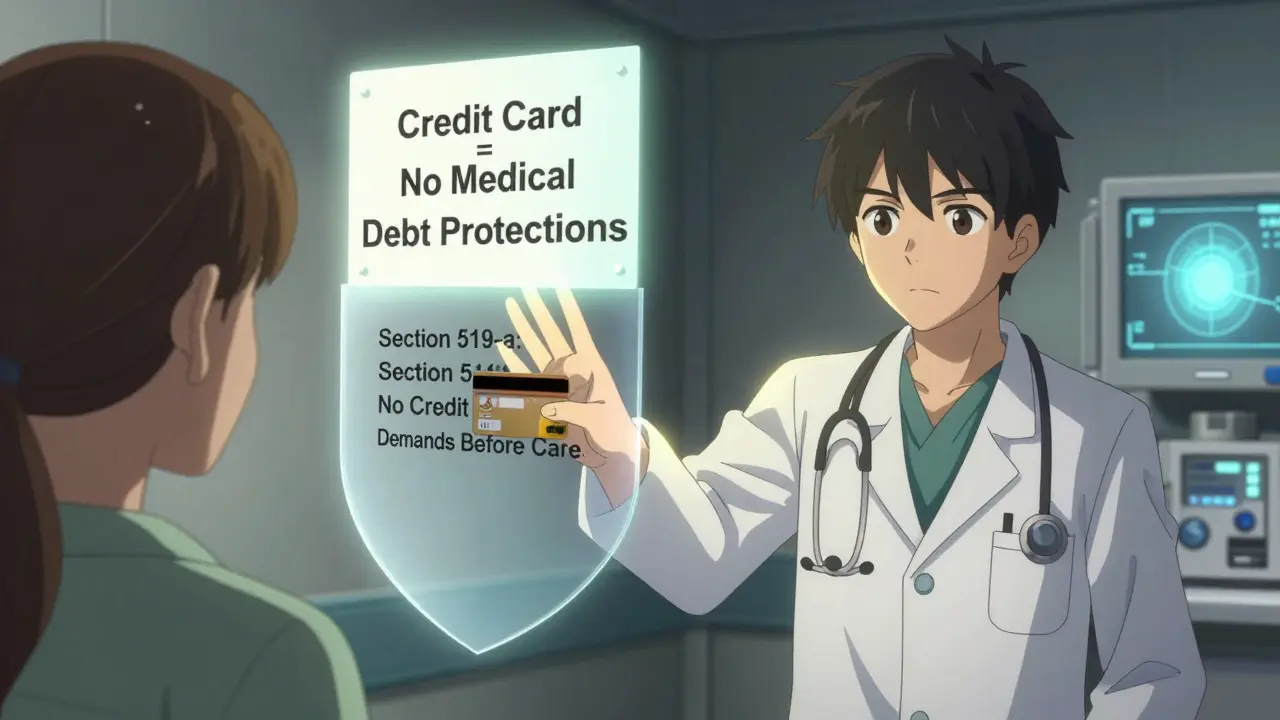

Credit Cards Before Care? Not Anymore

Here’s one of the most shocking practices: hospitals and clinics asking for your credit card before giving emergency care. Or keeping your card on file. Or requiring preauthorization just to treat you for a broken arm or a severe infection.

General Business Law Section 519-a puts a hard stop to that. Providers can no longer demand credit card information before providing emergency or medically necessary services. Period. And if they do, they’re looking at a $5,000 fine per violation.

But there’s another layer. The law also requires providers to clearly warn you if you pay with a traditional credit card. Why? Because only debt from healthcare-specific financing products (like CareCredit®) gets protected under state and federal medical debt rules. If you use your Visa or Mastercard, you lose those protections. That means:

- Your medical debt can still show up on your credit report

- Collection agencies can sue you

- Wage garnishment and liens on your home are still possible

With healthcare financing products? None of that. The CFPB’s 2024 rule removed medical debt from credit reports entirely-but only if it came from a medical financing product. Traditional credit card debt? Still fair game.

So if you’re told, “We need your card now,” say no. If you’re forced to pay with a credit card, ask for a written warning about the risks. They’re legally required to give it to you.

How This Compares to Federal Law

You’ve probably heard of the No Surprises Act, which took effect in January 2022. That law stops you from getting surprise bills from out-of-network providers. If you go to an in-network hospital but get treated by an out-of-network anesthesiologist? You’re protected. You pay in-network rates.

But the No Surprises Act doesn’t touch how you pay. It doesn’t stop providers from asking for your credit card upfront. It doesn’t require separate consent. It doesn’t stop them from steering you into CareCredit®.

New York’s laws go further. They target the hidden financial traps inside in-network care. That’s why experts call New York’s approach the most aggressive patient financial protection framework in the country. It’s not just about surprise bills-it’s about how you’re forced to pay for care.

And it’s working. Since these laws took effect, complaints about medical debt collection have dropped 18% in New York, according to state health data. Patients are finally starting to understand their rights.

What This Means for You

If you’re a patient in New York, here’s what to do right now:

- Ask for separate consent forms for treatment and payment. Don’t sign anything that combines both.

- If someone tries to help you fill out a financing application, say no. Fill it out yourself.

- If you’re asked for a credit card before emergency care, refuse. You have the right to treatment without payment upfront.

- If you pay with a credit card, ask for the written risk notice. Keep it.

- If you’re pressured or misled, file a complaint with the New York State Department of Health.

If you live outside New York? Pay attention. These laws are a blueprint. States like California, Illinois, and Massachusetts are already drafting similar bills. The federal government is watching. The Consumer Financial Protection Bureau has already removed medical debt from credit reports. That’s the trend.

Medical care should never come with a financial trapdoor. You’re not a credit risk. You’re a patient. And the law is finally catching up.

Why These Laws Are So Important

Let’s put numbers to it. In 2022, 74.6 million Americans had medical debt. By 2023, that number jumped to over 100 million people holding $195 billion in medical debt. That’s not just bills-it’s ruined credit scores, lost homes, and delayed care because people were too scared to go to the doctor.

These laws don’t just change paperwork. They change power. They shift control from providers and lenders back to patients. They stop the system from treating illness as a financial opportunity.

And that’s why this matters. It’s not about New York. It’s about what’s next.

Do these laws apply to me if I don’t live in New York?

Yes, indirectly. While these laws are specific to New York, they set a national precedent. Other states are already copying them, and federal agencies are watching closely. The CFPB’s move to remove medical debt from credit reports and the No Surprises Act are part of the same trend. Even if you’re not in New York, you’re likely to see similar rules in your state soon. Know your rights now-because they’re coming.

What if a provider refuses to give me separate consent forms?

You have the right to walk away. If a provider won’t follow the law, you can file a complaint with the New York State Department of Health. Even if enforcement is paused, your complaint creates a record. If enough patients report violations, it forces action. You’re not just protecting yourself-you’re helping change the system.

Can I still use CareCredit® or other medical financing?

Yes, but only if you apply for it yourself. Providers can’t help you fill it out, suggest you use it, or push you toward it. You can still choose to use it, but you must do so with full understanding. Read the terms. Ask about deferred interest. Know that if you miss a payment, you could owe years’ worth of interest all at once. It’s legal-but make sure it’s smart for you.

Why does paying with a credit card remove my protections?

Because federal and state medical debt protections only apply to debt created through healthcare-specific financing products. If you use a Visa or Mastercard, the law treats that like any other consumer debt. That means collectors can sue you, garnish your wages, or report it to credit bureaus. If you use CareCredit®, those protections kick in. That’s why providers are required to warn you-so you can choose wisely.

Are there penalties for providers who break these laws?

Yes. Violating the consent law (Section 18-c) can cost $2,000 per incident. Violating the financing or credit card rules (Sections 349-g and 519-a) can cost up to $5,000 per violation. These aren’t small fines. They’re designed to make non-compliance too expensive to ignore. If you see a violation, report it. Your report could prevent others from being exploited.

Joe Prism

March 5, 2026 AT 05:06Finally. The system was built to exploit vulnerability. Medical care shouldn't come with a credit check.

These laws don't just protect-they restore dignity.

It's not about money. It's about consent.

And autonomy.

And basic human rights.

Simple.

Why did it take this long?

Bridget Verwey

March 7, 2026 AT 03:28Oh wow. So now they can’t sneakily sign you up for CareCredit like you’re a kid at a carnival game? Genius.

And you have to fill out the form yourself? Like, with your own hands? What a radical concept.

Next up: doctors asking if you want a bandage before slapping one on.

Also, I’m filing a complaint just for the vibes.

🫡

Andrew Poulin

March 8, 2026 AT 22:22Stop pretending this is revolutionary. This is basic. You don’t need a law to say don’t lie to sick people.

Providers have been scamming patients for decades.

These laws are just the bare minimum to stop the bleeding.

And if enforcement is paused? Good. Let them keep breaking the law until they get fined into submission.

They’ll listen when it hurts their bottom line.

Not before.

Weston Potgieter

March 9, 2026 AT 13:04Look I get it. You want to protect people.

But let’s be real.

Most folks don’t read anything anyway.

They sign the form because they’re in pain.

They pick CareCredit because they’re broke.

And they’ll still do it even if you hand them a golden ticket with glitter and a hug.

Law changes nothing.

People change.

And nobody’s changing.

Just more paperwork for people who already hate paperwork.

Vikas Verma

March 10, 2026 AT 20:07As a global healthcare professional, I commend New York's regulatory framework.

This paradigm shift aligns with WHO’s ethical governance principles.

Financial coercion in clinical settings is a systemic violation of patient autonomy.

Implementation requires cultural adaptation.

India’s private healthcare sector exhibits similar predatory patterns.

Replication of consent architecture is imperative.

Training protocols must be standardized.

Penalties must be non-negotiable.

Let this be the first domino.

Sean Callahan

March 11, 2026 AT 00:10so like… you can’t ask for a card before emergency care? wow.

what a shocker.

i mean… who even does that?

oh right. EVERYONE.

and now they’re fined 5k? cool.

so… what happens when you go to the er and they say ‘we need your card or we can’t treat you’?

do you just… leave?

do they call the cops?

or do you just die on the floor?

…i think i’m gonna need a lawyer just to breathe.

Ferdinand Aton

March 11, 2026 AT 05:47Wait, so now you have to fill out your own financing form? That’s like… a civil rights win?

What’s next? Hospitals can’t make you stand in line?

And you can’t be forced to use CareCredit?

Man, I thought we were already past this.

Maybe we should just give everyone free healthcare and be done with it.

William Minks

March 12, 2026 AT 09:49YES. FINALLY. 🙌

They can’t help you fill out CareCredit anymore? YES.

I’ve seen nurses do it. It’s sneaky. It’s manipulative.

And now? You have to do it yourself.

That’s power.

That’s dignity.

And yeah… I’m telling all my cousins.

Share this. Please. 🙏❤️

Jeff Mirisola

March 13, 2026 AT 20:14This is what real reform looks like.

Not just patching holes.

But rebuilding the foundation.

Medical debt isn’t a personal failure.

It’s a design flaw.

And New York just rewrote the code.

Other states? You’re watching.

And you’re next.

Keep going. Don’t stop.

We’ve waited too long for this.

Susan Purney Mark

March 14, 2026 AT 07:26I work in a clinic. I’ve seen patients cry because they didn’t understand the CareCredit terms.

They thought ‘no interest for 12 months’ meant ‘no interest ever’.

Then they got hit with $3,000 in back interest.

One woman didn’t come back for her chemo because she was scared of the bill.

These laws? They’re not paperwork.

They’re lifelines.

Thank you, New York.

I’m crying right now.

💛

Ian Kiplagat

March 15, 2026 AT 20:47Interesting. The UK has no equivalent.

Medical debt is rarely reported here.

But financing schemes? They’re everywhere.

Private clinics push ‘payment plans’ like subscriptions.

Same trap.

Maybe this model should be exported.

Not just copied.

Adapted.

With teeth.

Amina Aminkhuslen

March 15, 2026 AT 23:41Oh honey. You think this is a win?

Let me tell you what really happens.

Providers just switch to ‘donation’ forms.

Or ‘voluntary payment agreements’.

Or ‘community support initiatives’.

They’ll rename the trap and call it ‘care’.

And patients? They’ll still sign.

Because they’re desperate.

And scared.

And tired.

And they don’t know the difference anymore.

This law? It’s a Band-Aid on a hemorrhage.

amber carrillo

March 17, 2026 AT 10:17As someone who’s been through medical debt, I can say this: consent isn’t a form.

It’s a conversation.

And too many providers treat it like a checkbox.

These laws force them to pause.

To explain.

To listen.

That’s the real victory.

Not the fine.

Not the form.

But the moment someone stops rushing you.

And asks if you’re okay.

That’s healing.

And it’s long overdue.